Chapter 3: An Overview of Options Strategies

Most of the hedges described in this book are options structures. They rely upon buying and selling combinations of calls and puts with different strikes and maturity dates. We are mainly concerned with uncovering strategies that provide protection at low cost. In this chapter, we provide a non-technical overview of options, in preparation for the hedges we will dissect in Chapters 4 and 5. We make no effort to derive Black–Scholes or any other pricing formula. Rather, we will use the Black–Scholes formula as a way to adjust for different strikes and times to maturity. Value will be expressed in the currency of implied volatility. Normalising across strikes and maturity dates can help us decide which options are rich and which are cheap. We start with a bare-bones description of puts and calls, then transition into more complicated structures, such as spreads, butterflies and ratios. Our ultimate goal is to identify horses for courses, i.e. hedging structures that are well suited to a particular market environment. It will take some time before we can delve into regime-specific analysis. This chapter serves as necessary background material. Note that we will primarily focus on exchange-traded futures and options, as they are easier to analyse and trade at an accurate and timely price.

Options contracts have a long and varied history, possibly extending back to ancient Greece and carrying on through to England in the 1600s and the US thereafter. It may be that the options market took off when corporations started to add sweeteners to stock and bond issues. For example, in the 1840s, the New York and Erie Railroad Company issued one of the first recorded convertible bonds. The bonds could be exchanged for, or “converted” to shares if the stock price went up enough. In other words, there was a call option embedded in the bond. This was attractive to the company as the bonds could be floated at relatively low yield. At the same time, investors were keen to own bonds that offered participation in a rising market. New instruments have the greatest chance of success if they generate an active two-way market. There are natural buyers and sellers of the contract. Today, calls and puts represent a tug-of-war: between hedgers who need to insure existing portfolios, and speculators who want to take a directional punt or trade volatility.

THE BUILDING BLOCKS: CALLS AND PUTS

We need to use a bit of math in this section, to make the concepts clearer. Derman (1996) has remarked that Fischer Black wanted an introductory article about the Black–Derman–Toy model to be written without any formulas, with a focus on developing the necessary intuition. While we have fallen short of Black's ideal in this chapter, we will try to minimise our use of complicated formulas and equations. There is an entire industry devoted to exactly that and we have no intention of re-inventing the wheel. The reader might want to consult Wilmott (2013) for a more mathematically minded, yet pragmatic, treatment of options theory. For now, let's start with calls and puts, as these are the most basic exchange-traded options.

Readers with a strong background in options strategies can comfortably jump to the section “Skew Dynamics for Risky Assets” later in this chapter.

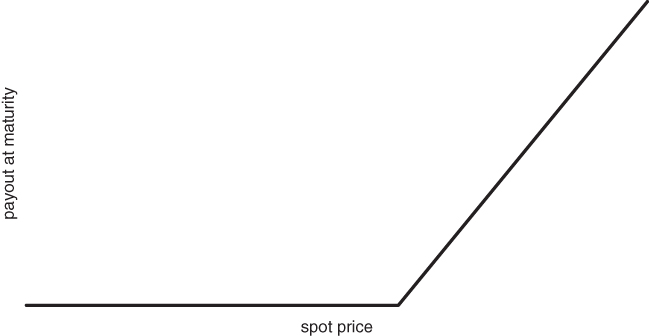

Calls and puts are financial contracts with standardised features. The owner of a call has the right to buy an asset at a predetermined price X at maturity. X is called the option strike. The owner of a put has the right to sell an asset at the predetermined price X. However, in either case, there is no obligation to do so. In practice, you would only buy an asset at price X if the market price S(t) > X. Otherwise, you could just buy the asset at a lower price in the market. In effect, you are hoping for a rally above the strike. Similarly, you would only sell at X if S(t) < X. Viewed in isolation, calls represent bullish bets and puts represent bearish ones. Outright call owners would like nothing more than for the price of the underlying asset to skyrocket from now to time T. This would allow them to buy at X and then dump the asset into the market at a much higher price. The payout of a call at maturity is given in Figure 3.1.  Figure 3.1 Payout shape for a call option at maturity

Figure 3.1 Payout shape for a call option at maturity

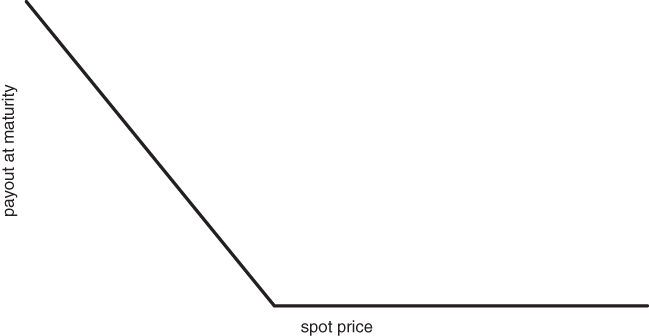

Puts generate a positive payout for whenever the spot drops below the downside strike as shown in Figure 3.2.  Figure 3.2 Payout shape for a long put at maturity

Figure 3.2 Payout shape for a long put at maturity

It's worth reflecting on the hockey stick payouts for a while, as the bendy part of the curve is what makes options interesting and important. In both cases, the discontinuity in the slope of the curve occurs at the strike X. While options traders generally do not hold to maturity, the terminal payout has a large bearing on the way a call or put evolves over time. We use calls as our base case for now. The value of a call at maturity is . You receive the higher of the asset price minus the strike and 0. This quantity is also called the terminal payout of the call. This implies that, once you have bought the call, your maximum loss is 0, while your potential gain is theoretically unlimited. This does not mean we are suggesting that you will always make a profit from the trade. You need to overcome the initial cost of the call to bank the profit.

Similarly, the value of a put at maturity is . The kink in the payout at introduces a non-linearity into the payout curve. Why is this important? It allows the owner of a call or put to benefit from large and unexpected market moves. The wider the range of outcomes for , the greater the payout potential of a call or put. Since losses are strictly bounded, put and call prices should increase in tandem with uncertainty. In the unorthodox and evocative language of Taleb (2012), puts and calls are “anti-fragile”. They profit from disorder. The wilder and more unpredictable becomes, the better. We can illustrate this idea using a simple example. The example relies upon a single “binomial” outcome, generated by the flip of a coin.

- Suppose we buy a call option on a stock currently trading at 100 and make some assumptions about where the stock can go.

- There are two scenarios. In the first, there is a 50% chance that the stock will land at 90 and a 50% chance the stock will land at 110 at time . In the second, the spread is wider. There is a 50% chance that and a 50% chance that . In Figure 3.3, we sketch the two scenarios in tandem.

Figure 3.3 One-step binomial model with variable volatility

- The expected value of in both cases, e.g. . However, the call is worth in scenario 1 and worth 10 in scenario 2. Scenario 2 has a higher scenario-averaged payout for the owner of the call and hence should be worth more.

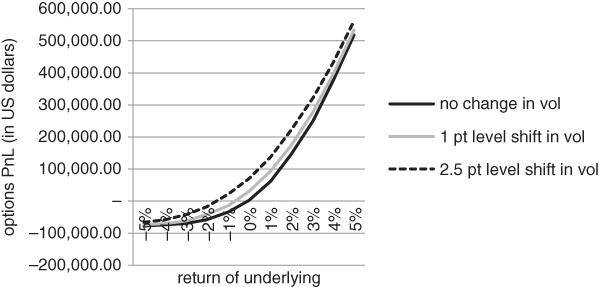

This strongly suggests that call and put prices go up as the perceived range of outcomes increases. If we replace the discrete price tree with a continuous return distribution, the situation is identical. Let's take the simplest continuous case, where returns are normally distributed. Recall that a normal distribution is completely specified by two parameters, its mean and standard deviation. Returns fall under the classical “bell curve” after repeated experiments. In this case, uncertainty is completely encoded in the parameter σ. If we normalise the standard deviation appropriately, to adjust for variation over different time horizons, we wind up with something denoted by σ. σ is familiarly called the volatility of returns. It is an extremely important quantity, as it measures risk at the most basic level. The price of both a call and put is increasing in volatility. Without demonstrating anything, we have graphed the payout curve of a call option for different volatility levels in Figure 3.4.  Figure 3.4 Sensitivity of Bund calls to changes in volatility

Figure 3.4 Sensitivity of Bund calls to changes in volatility

For the sake of concreteness, we have focused on German Bund futures options in Figure 3.4. A call option on any underlying would have the same qualitative payout profile.

Since the payout profile of a call or put is going to converge to a piecewise linear function at maturity, it needs to become increasingly curved at the strike along the way. Note that a piecewise linear function is just a collection of straight lines glued together.

The non-linear payout creates some complexity. An option can respond in a variety of ways to small changes in , depending on where is relative to . If is far below , a call will display almost no sensitivity to the spot. The payout curve is simply too flat there. On the other hand, if is far above , the call will move nearly in tandem with the underlying price. Later, we will discover that the variable exposure in an option can cause the dynamics of a hedging structure to change quite dramatically over time. We need to understand the chameleon-like characteristics of basic or “plain vanilla” options before we can come to grips with more complicated hedging structures.

The way that a fixed option responds to changes in price and time to maturity can be highly variable. How can we quantify the amount an option will move if we perturb , or other factors that might determine the price of an option? Perturbing means that we are only moving it by a small amount. It's a mathematical term with far ranging implications. If you slightly change the parameters in a system, does it matter? The direct approach to perturbation analysis involves calculating the so-called “Greeks”. The Greeks locally measure the sensitivity of an option to various factors. For larger moves in the spot or another quantity, option prices can move far more than the commonly used Greeks would predict. Assume that we have a formula for pricing calls and puts. Later in this chapter, we will introduce the Black–Scholes pricing model, but any formula will do for now. If we use a different convention from the market, our Greeks might be different from the market's, but they will still be well-defined. If we want to estimate sensitivity to , we just perturb then re-price the option to calculate the slope of the payout curve at . This tells us how much our call is likely to move for a small change in the price of the underlying. This slope is called the option delta, in particular, . is the size of the perturbation. Mathematicians like to supply emotional content to seemingly dry functions and equations and we take their lead here. The reason that Δ is unambiguously defined is that C is “well-behaved” as a function of S, at least until maturity. The slope of C as a function of S never blows up, no matter how small might be. Analogously, we can estimate C's sensitivity to σ. We have already seen that puts and calls benefit from confusion, disorder and uncertainty and quantify this notion below. σ, the volatility of S that is agreed upon by the market, compresses these diverse notions of risk into a single number. If we rewrite C(S) as C(S, σ), we can define vega by perturbing σ for fixed S, then calculating the slope. Theta, θ, refers to the time decay of an option. It is formally defined as for a call and for a put. The convention is to set dt equal to 1 day, so that θ measures how much you will lose in a day if nothing happens. For most options, delta, vega and theta play a significant role. At the extremes, other Greeks can come into play. Close to maturity, gamma can play a large role. Gamma, γ, is sometimes called the “delta of delta”, as it measures the degree to which delta changes for a small change in the spot. In particular, .

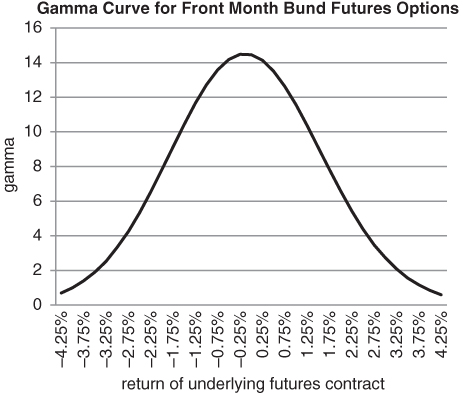

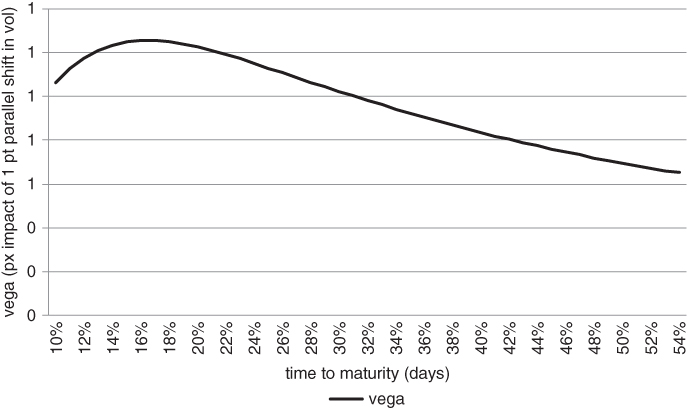

If γ is small, the payout function is locally quite straight. Risk varies almost linearly as a function of the spot price. Conversely, the profit/loss in a high gamma option can change quite dramatically as the spot moves. Short-dated options that are close to ATM have relatively high gamma, as we can see in Figure 3.5.  Figure 3.5 Bell-shaped gamma curve as a function of underlying return

Figure 3.5 Bell-shaped gamma curve as a function of underlying return

As time to maturity increases, the importance of gamma diminishes. Long-dated options have fairly flat payout profiles across all spot values. Rho, ρ, takes the place of γ as a significant Greek. Specifically, ρ measures the sensitivity of an option to changes in the discount rate.

The reader may wonder why we have made no mention of other higher order Greeks, such as volga (the sensitivity of vega to small changes in implied volatility). Since we are only dealing with combinations of calls and puts in this book, most of the higher order Greeks are tiny. We are avoiding bank creations such as barrier and knock options, where there can be a discrete jump in the payout at maturity. From a hedging perspective, we don't need to have a very precise handle on the Greeks. We only require that our hedging structures have enough kick for a large move in the underlying.

An option is European style if you are only allowed to exercise at maturity. It's American style if you can exercise at any time up to and including maturity. This has nothing to do with where the option or underlying asset is based, e.g. options on German Bund futures have American style delivery. Stock indices and the VIX generally have European style exercise, while options on futures or individual stocks tend to be American. This is not entirely arbitrary. The cash settled options are the European ones. Otherwise, exchanges would have to issue official settlement prices for every index on a daily basis. The settlement prices would determine how much would be credited or taken away from a client's brokerage account. This would be cumbersome and subject to manipulation. There is also the question of valuation. At first sight, it seems reasonable that an American call or put should be worth more than a European one with the same strike and time to maturity. You have the freedom to exercise whenever you want. This “optionality” should be worth something. In other financial contexts, it generally is. For example, Silber (1991) has estimated that a restricted stock should trade at a roughly 50 basis point per annum discount to an equivalent stock that can be traded freely.

Here, it turns out that (in the absence of dividends or other technical factors) the American exercise feature is generally worthless. Imagine that you own an American style call that is in the money, i.e. . You could exercise the call if you wanted to, receiving after selling the stock back into the market. The trouble with this strategy is that the call should be worth more than at the time of exercise. The position is equivalent to a long position in the spot, with a purchase price of X, combined with a long put struck at X. Since the embedded put has positive value, you would be well served to sell the call back into the market rather than exercising the option.

WHY BUY A CALL OR PUT?

“Why” can be a dangerous question to ask in many contexts, but is an important one here. There are numerous reasons to buy a call or put, with varying degrees of sophistication. The most basic reason to buy an option is that you have to. You either need to block out unpalatable scenarios in your core portfolio or you want to add a new position, but are unable take on too much additional risk. Buying puts on the S&P 500 to protect against further losses in a traditional equity portfolio is a forced move. You want to maintain your existing portfolio but need to hedge against disaster. Buying puts on the target stock in a potential merger, on the assumption that the deal won't go through, is something entirely different. Here, you want concentrated exposure to a low-probability event. If the deal goes through, you only lose the premium you have paid. On the other hand, if the deal breaks, the stock will probably crater. You might then make many multiples of the original premium paid. In these cases, you might not worry or even know whether the puts are overpriced at the time of purchase. All you care about are the payouts under various scenarios.

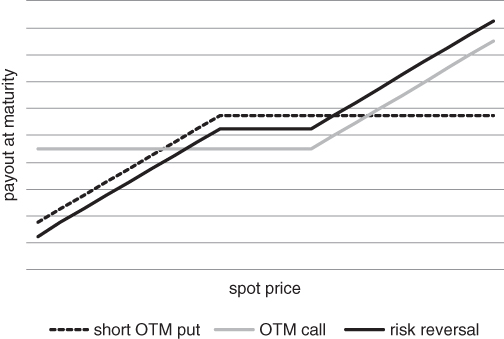

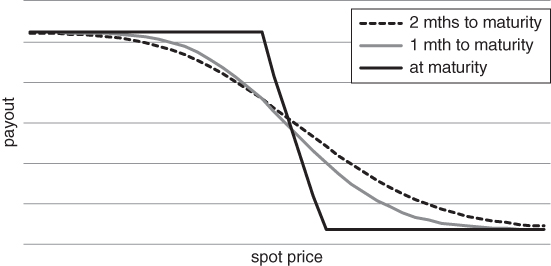

This can create opportunities for volatility arbitrage traders, who are always sniffing around for mispriced options. Volatility is their currency, not price. If they find something, they will try to extract a profit from the discrepancy between an option and some combination of other options and the underlying asset. Another reason to buy an outright call or put is to express a hybrid view on direction and volatility. You might be able to harvest a bit more alpha by trading an option rather than the underlying. Let's say you want to generate long exposure to emerging market equities. The most liquid instrument available is an emerging markets ETF. You could buy the ETF, buy a call or sell a put. When you buy a call, your potential profit is unbounded but a move needs to occur reasonably quickly. As time passes, the call gradually loses value. Selling a put requires less conviction but an equal dose of courage. If markets stabilise, the short put strategy is likely to perform well. You are betting that any sell-off is going to be more than compensated by the premium you have collected. However, if the price of the ETF crashes through your put strike, you are left with a fully exposed long position. Buying a call is a punchier play, predicated on the idea that the market has underpriced the probability of a large upside move. However, if nothing happens, you lose the premium paid. Buying a put can be a defensive or speculative bear market play. A speculative downside put can be statistical in nature, even if it's not a relative value play. You are simply arguing that the market has underpriced the probability of a move toward the downside strike. If you are really bullish, you can buy a call and sell a put. This structure is usually called a risk reversal. Since a long call and short put both have positive delta, the risk in each leg compounds the risk in the other. Figure 3.6 shows a payout for a risk reversal. Since we have sold an OTM put and bought an OTM call, the strikes are spaced apart. As we push the put and call strikes closer together, the structure converges to a forward contract.  Figure 3.6 Construction of a split-strike risk reversal

Figure 3.6 Construction of a split-strike risk reversal

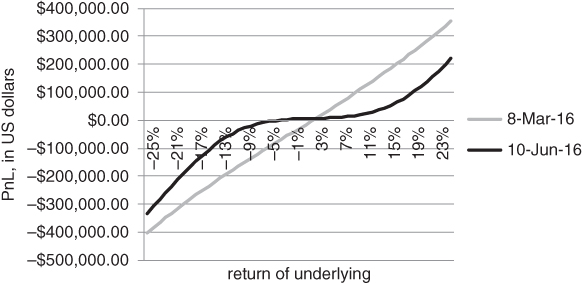

Figure 3.7 refers to a split-strike risk reversal on the iShares MSCI Brazil ETF. We sold 1,000 puts and bought 1,000 calls on March 8, 2016 and wanted to get a handle on the payout curve roughly 3 months thereafter. The curve evolves from a nearly linear shape (with delta close to 0.5 ) to one that is fairly flat in the middle.  Figure 3.7 Evolving payout of a risk reversal on the iShares MSCI Brazil ETF

Figure 3.7 Evolving payout of a risk reversal on the iShares MSCI Brazil ETF

Suppose there is a persistent put skew in the market you are trading. Put skews are characteristic of risky assets, such as equity indices, based on asymmetry in the underlying return distribution and excess demand for hedging downside risk. “Risky assets” have a positive expected return over the long term (at least according to theory), but may be exposed to large negative downside surprises. When there are more large negative surprises than positive ones, the underlying distribution is said to be skewed to the downside. You then collect premium if the put and call strikes are the same distance from the ATM strike. In other words, you get paid up front to hold the structure. Alternatively, you can construct costless risk reversals where the put strike is considerably further away from the money than the call strike. By “costless”, we mean that you collect the same amount of premium from the put as you pay for the call. In the limiting case where the call and put have the same strike, you have effectively bought a forward contract. Your position will move contiguously with the underlying price and is insensitive to changes in volatility. It turns out that vega in the put cancels out the vega in the call. The put–call parity formula shows that buying a call and selling a put with the same strike and maturity generates a structure that is linear in . Namely, if and are calls and puts with the same strike and time to maturity, then  where and are the spot price of the underlying asset, the discount rate and the strike, respectively. We can rewrite the formula as

where and are the spot price of the underlying asset, the discount rate and the strike, respectively. We can rewrite the formula as  Since the current price and don't depend on the volatility of , we can essentially create a forward with a long call and short put (i.e. risk reversal) structure. Whenever there is a liquid futures contract, there is probably no point in buying a call and selling a put with the same strike. Given the proliferation of options on ETFs that have no equivalent futures, however, there are many cases where building a synthetic forward is a reasonable idea. The forward allows you to apply leverage as well as minimise interest and dividend income.

Since the current price and don't depend on the volatility of , we can essentially create a forward with a long call and short put (i.e. risk reversal) structure. Whenever there is a liquid futures contract, there is probably no point in buying a call and selling a put with the same strike. Given the proliferation of options on ETFs that have no equivalent futures, however, there are many cases where building a synthetic forward is a reasonable idea. The forward allows you to apply leverage as well as minimise interest and dividend income.

Forwards, as we know, are “delta one” instruments. There is no kink in the payout curve, hence vega is always 0. Whenever there is a liquid futures contract, there is probably no point in buying a call and selling a put with the same strike. Given the proliferation of options on ETFs that have no equivalent futures, however, there are many cases where building a synthetic forward is a reasonable idea. The forward allows you to apply leverage as well as minimise interest and dividend income.

Once we move beyond these basic structures, we can create a diverse range of hedging structures by mixing options with different strikes and times to maturity. However, we need to have some notion of relative value before we can decide which structures look promising. We need some way to place all of the available options on a single underlying on an equal footing. This motivates our discussion of the Black–Scholes equation in the next section.

For now, it is probably worth reviewing the concept of “money-ness” for an option. We will repeatedly use the acronyms ATM, ITM and OTM in what follows and need to specify what these mean. A call or put is at-the-money, or ATM, if the spot price roughly matches the strike. Why do we use the word “roughly” in a definition? There is some ambiguity when defining money-ness. One approach is to say that the ATM option strike exactly matches the spot price. But what if we are dealing with an option on a futures contract? The Black 76 formula prices calls and puts using the current futures price. This suggests the alternative that an ATM option's strike should match the equivalent maturity forward. A third definition, which closely matches the forward price one, specifies that the strike whose delta is closest in magnitude to 0.50 is at-the-money. Once we have decided what we mean by an ATM option, out-of-the-money OTM and in-the-money options follow naturally. OTM calls have a strike higher than the ATM strike and OTM puts have a lower strike. Generally speaking, OTM options have no intrinsic value. They would expire worthless if the maturity date were today.

THE BLACK–SCHOLES EQUATION AND IMPLIED VOLATILITY

In 1973, Fischer Black and Myron Scholes published a landmark paper called “The Pricing of Options and Corporate Liabilities”. The paper appeared in the Journal of Political Economy (1973) , of all places. They derived a partial differential equation for the value of a “warrant”, or call option, using two different approaches. One approach relied upon replicating the option using a dynamic hedging strategy. The other applied the Capital Asset Pricing Model (CAPM) to map risk onto expected return. As it turned out, this equation was solvable, leading to the Black–Scholes formula. Black was able to draw upon his technical background and identify the equation as one that models the diffusion of heat through a metal rod.

Countless books and articles have analysed the Black–Scholes equation from a mathematical and historical perspective and we will make no effort to reinvent the wheel. We simply point the reader to the original paper and Mehrling's fascinating biography of Fischer Black (2005) for further details. Haug (2009) is also worth consulting, for an alternative history of option pricing. Specifically, the price of a European call option is given by  , where

, where and .

and .

Here, gives the probability that a normally distributed random variable is less than and takes values between 0 and 1. Recall that a European option can only be exercised at maturity. Options with more complicated features usually can't be priced using a simple analytic formula.

We call the reader's attention to a comment about the formula in the original paper. (Note that the expected return on the stock does not appear in (the) equation. The option value as a function of the stock price is independent of the expected return on the stock.)

The comment almost looks like a throwaway, but it would be hard to overemphasise its importance. If depended on the expected return of , the Black–Scholes formula would contain two unobservable quantities, namely and . Note that and have unambiguous market prices and X and are explicitly defined by the option contract. They are all known precisely. Since has no impact on , we can uniquely solve for given a market price for . This allows us to view Black–Scholes as a powerful translation device, converting option prices into implied volatilities. Options with different strikes and maturities can be placed on an equal footing. German Bund futures, for example, have hundreds of listed options at any given point in time. The same is true for major equity indices, short rates, commodities and individual stocks. For each underlying asset, there is a multitude of different strikes and maturity dates. If we try to compare their prices, we will get hopelessly lost. So how do we specify which options might be relatively cheap and expensive? This is where the Black–Scholes formula comes to the rescue.

We observe that and are increasing in . All things being equal, the higher the volatility of an asset, the higher its option price. The reason for this is straightforward and has been touched upon previously. When we buy a call, our payout at maturity is . While there is lower bound on the payout, potential gains are unlimited. Our loss is capped at the premium we have paid. As volatility increases, the range of outcomes also increases. This raises the odds that will be large and positive, implying that the expected value of should go up. This means we can solve for σ uniquely given the market price of a call or put. In particular, or for a call and put, respectively. Volatility is a deterministic function of the option price, spot price, strike, risk-free rate and time to maturity. This allows us to compare options with different strikes and maturities in a sensible way. It is hard to develop a visceral feeling about the price of an option, i.e. what does it mean for a 1-month 2050 put on the S&P 500 to have a price of 25? How much of the price is intrinsic value, how much is premium and how does the premium scale as time increases? (Note that the intrinsic value of an option is the amount it would be worth if it expired today.)

However, if someone told you that the implied volatility of that put were 14 (really 14%, though volatility is usually quoted in percentage points), you would have something solid to go by. Is the implied volatility higher than 30 day trailing realised volatility? Is it much higher than ATM implied volatility? Where is it trading relative to 3-month implied volatility? These sorts of questions allow us to say something about the fair value of the 2050 put, in relative terms.

THE IMPLIED VOLATILITY SKEW

When we use the Black–Scholes equation to convert the price of an option into an implied volatility, there is some model misspecification involved. Black–Scholes assumes that the volatility of the underlying asset is constant, i.e. independent of time and level. It prices options based on some kind of average volatility of the asset over the life of the option, with no regard as to where volatility is likely to be if the asset drops –20%. Yet, when we derive different implied volatilities for options with different strikes, we are contradicting the model by saying that volatility is level-dependent after all. Does this obviate the possibility of using the model at all? Most practitioners would argue not. As we discussed above, the model provides a powerful method for converting option prices into a quantity that we can understand and trade. Suppose that the S&P 500 is trading at 2100 and the implied volatility of the 3-month 1750 put is 10 points higher than for the 3-month ATM put. The market is warning us that volatility will go up quite dramatically if the index gets anywhere near 1750. We can think about this in another way. Investors are coming up with realistic OTM option prices by fudging the only unobservable quantity in the formula. It is only natural that financial engineers wanted to put this on a firmer foundation over time. What started as a back-of-the-envelope calculation has progressively become more sophisticated. The idea of converting option prices into forward risk estimates is encapsulated in the concept of local volatility. We will not cover local volatility in this book and point the reader in the direction of Gatheral(2006).

For our purposes, level-dependent volatility is important as a mechanism for generating fat tails in the return distribution. If volatility jumps whenever an index drops below a threshold, the probability of even larger moves from that point will be greater than a normal distribution might predict. This may be related to contagion effects in the market, which we explore in Chapter 8. Here, we make no effort to solve the so-called “inverse problem”, where we infer market expectations about volatility from the price of various options on the underlying. As crisis hedgers, we are not operating in the domain of accurate calibration and prediction, but in the world of survival. Precise relationships can break down when the market suddenly shifts into a risk-off phase.

HEDGING SMALL MOVES

Suppose you have sold a call. The position is exposed to a sharp rise in the spot. You can hedge this risk in various ways. The same ideas apply if you've sold a put and the spot craters. There are two basic ways to manage risk if you have sold a put or a call. You can delta-hedge with the underlying asset or you can hedge the option with other options. In this section, we focus on delta hedging. Let's say you have sold an equity index put. For simplicity, the index doesn't pay any dividends and interest rates are 0. Then the put price P depends on the index price , the strike , the time to maturity and the implied volatility . In other words, we can write as . There's no reason to worry about how to price P for now. We can simply assume that the Black–Scholes formula is valid. It's then possible to calculate the delta of the put. The put delta tells you how much P is likely to move if the index S moves a bit. You can approximate the delta by repricing the put for a slightly different index value delta_S then calculating . In mathematical terms, you're calculating the partial derivative of P with respect to S. So if the put has a delta of –0.50 (traders would say this is a 50 delta put), you expect to lose 50 basis points if the index goes up by 1%. The delta of a put ranges from –1 to 0 and the delta of a call falls in the range from 0 to 1. Practitioners usually multiply by 100 when they tell you what the delta of an option might be. For example, a put with a delta of –0.50 would be called a “50 delta” put. It's clear that the delta must be negative, since we're dealing with a put. This implies that, for every 10 options you are short, you should be short 5 futures to immunise your position. On average, the profit from regular delta hedging should be dependent on the difference between the option's implied volatility at time of entry and the realised volatility of the asset. In theory, if you can consistently sell options at a higher volatility than the realised volatility of the underlying asset over the life of the option, you have the basis for a profitable strategy.

DELTA HEDGING: THE IDEALISED CASE

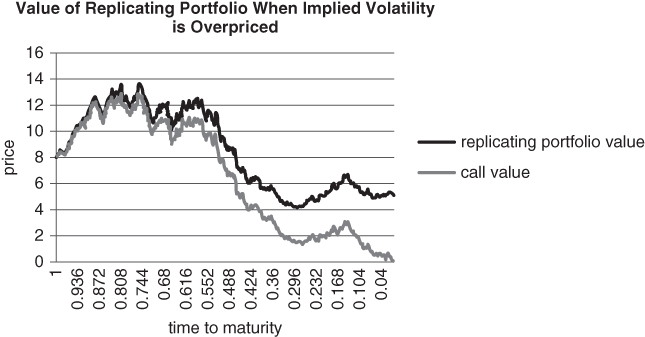

Suppose that you lived in an alternative reality where asset returns had normal distributions and volatility stayed constant. This might be a rough approximation of the way markets operate, but can be wildly off at the worst possible times. Suppose asset prices were driven by a random number generator whose properties could be easily inferred. In other words, the return-generating “machine” operated according to strict rules. You could trade at no cost or market impact and prices vibrated continuously through time. Some academics might equate this to a situation where everything was efficiently priced, as any inefficiency would be instantly stamped out by investors. However, this is not a necessary assumption. Here, we assume that statistical mispricings might still crop up in the options markets from time to time. Suppose we found an option whose implied volatility was higher than the constant realised volatility of the underlying. This might occur if the historical volatility of an asset over some interval were higher than the “true” volatility of the asset, by random chance. In this case, implied volatility might be linked to the abnormally high volatility in the past and hence overpriced. We could then turn an almost certain profit by selling the option and delta hedging with the underlying. The underlying asset would typically move less than the option predicted. This implies that the net asset value (NAV) of the delta-hedging strategy would decay more slowly than the premium in the option. It all sounds a bit fancy, so let's take a concrete example. The example is quite extreme, to illustrate the delta hedging concept. Suppose we have a 1-year call option on a stock. The call trades at a fixed 20% volatility, but the stock's realised volatility is a constant 10%. This is a mouth-watering opportunity, so long as the stock doesn't start going crazy. The stock is trading at 100, the call has strike 100 and interest rates are 0.

In Figure 3.8, we track the value of the call against the value of the replicating portfolio over time. Our strategy relies upon selling the call and delta hedging with the stock. In our example, we receive about 8 for selling the call and have to pay roughly 0.55*100 for the shares. Note that 0.55 is the call delta at the moment of sale. This implies we have to borrow roughly 47 from the bank to get the trade going. Over time, the borrow increases if we have to buy more shares and decreases if we sell them down. We can see that, for a representative path, the replicating portfolio decays much more slowly than the premium embedded in the call.  Figure 3.8 Extracting alpha from a call that is overpriced in implied volatility terms

Figure 3.8 Extracting alpha from a call that is overpriced in implied volatility terms

When you sell and delta hedge a call, the largest net profits are realised when the call quickly burns off. This was illustrated in the example above. In this happy case, you quickly gain on the call and subsequently don't have to hedge very much, as the call delta is now low. The delta burns off to the extent that hedging is unnecessary after a while. For a short put that is delta hedged, a rally in the spot is ideal. The less aggressively you need to hedge, the better.

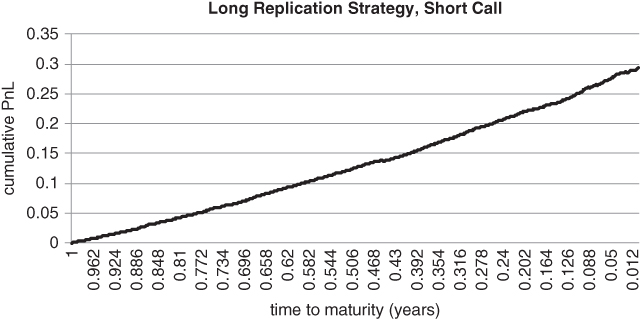

When an option is as mispriced as this one, the odds of locking in a profit are very high. You have a huge margin of error. In Figure 3.9, we simulate the performance of the replicating portfolio, short call strategy over a deliberately small number of paths. The terms are the same as in the example above. The graph tracks average profit as a percentage of the initial option price. After only 10 (!) simulations, our average profit evolves according to a very smooth line. If implied volatility is overpriced and the basic assumptions of replication remain intact, selling then delta hedging options should be an overwhelmingly successful strategy (see Figure 3.10). As we will find out, however, those can be giant “ifs”.  Figure 3.9 Arbitrage at its finest when implied volatility is severely mispriced

Figure 3.9 Arbitrage at its finest when implied volatility is severely mispriced  Figure 3.10 Impact of jumps on P&L

Figure 3.10 Impact of jumps on P&L

PRACTICAL LIMITS OF DELTA HEDGING

Once we loosen our assumptions a bit, it becomes harder to delta hedge with accuracy. We can't just sell options that appear to be overpriced and expect to hedge away all of the price risk in the underlying. Changes in volatility, discrete jumps and variations in price dynamics according to timescale will eventually lay siege to our plans. Physical time may appear to move continuously forward, at a constant rate. However, financial data appears discretely and prices can jump discontinuously (i.e. more than one tick) from one time stamp to the next. Some people equate high volatility to a “fast market” and this description feels about right. Fast markets truly give one a feeling of vertigo, like a roller coaster at the local theme park. When lots of transactions are occurring per unit interval, the perception is that time is actually whizzing along faster than normal. Ané and Geman (2000) have introduced the notion of a stochastic transaction clock to account for this phenomenon. When lots of transactions are hitting the wires, a fixed unit of time can contain an unusual amount of activity. By rescaling time, they are able to transform fat-tailed distributions into more normal looking ones.

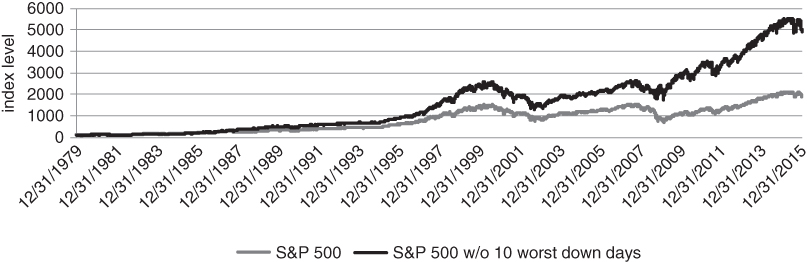

Let's revert from a paradigm that vaguely resembles Einstein's theory of special relativity back to standard clock time. Even if we haven't observed a six standard deviation drop in the recent past, the risk of such a move is always lurking beneath the surface. These moves are of great significance, even if they sometimes reverse themselves over time. To an options trader, intraday mega-moves can threaten survival. We can't quietly edit out moments where there is “blood on the streets”. Price jumps are a vital part of the signal and, over the long term, can be definitive. They are not products of measurement error, analogous to noisy patches on a digital image that need to be smoothed out. A small number of very large moves can have a surprisingly large impact on returns over a long horizon. If, for example, we remove the largest 10 down days for the cash S&P 500 index since 1980 as shown in Figure 3.11, the annualised return of the index goes from 8.26% to 11.17%.  Figure 3.11 Impact of removing 10 largest down days from cumulative S&P performance

Figure 3.11 Impact of removing 10 largest down days from cumulative S&P performance

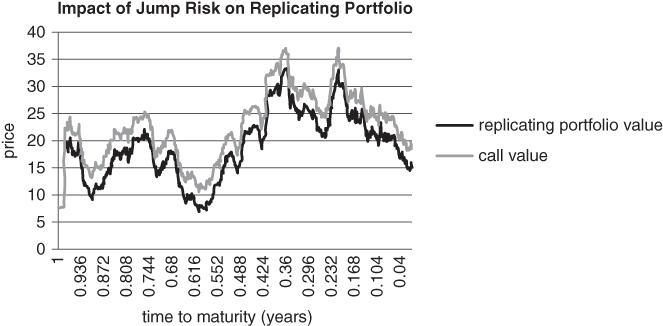

This is quite a remarkable statistic, as these down days only account for 0.11% of all trading days over the entire period! The index might eventually retrace to where it was before the devastating down move, but the damage has been done. Our delta hedging strategy would have been forced into the market, selling the underlying near the low then covering at the original level. In the following example, we show how a single price spike can ruin a delta hedging strategy. We return to the 100 strike call example, with a few modifications. Implied volatility (20%) is only slightly mispriced relative to realised volatility in the observable past. Realised volatility is set at 19%, so there is little margin for error. On average, we can extract alpha from the discrepancy in the idealised Gaussian world with no price impact or costs. However, a single price jump can ruin our plans. What is a “reasonable” price jump to consider? The black swan purists might argue that this is a silly question, with some justification. Once we depart from the world of normal distributions, spectacularly large moves are possible. Unreasonable looking moves can occur surprisingly often. In this section, however, we just want to show that it wouldn't take much of a jump to push the delta hedging strategy offside.

We start with an example that looks unremarkable from a long-range perspective. Financial historians are not likely to look upon October 2, 2015 as an extraordinary day and we have selected it for precisely that reason. The S&P returned +1.43%, which is less than a 1.5 standard deviation 1-day move. Returns of this magnitude should occur about 13% of the time for a normal distribution. These sorts of moves are quite common across equity indices, interest rates, currencies and commodities. Markets had been very turbulent in August and bearish in September. There was a great deal of anticipation for the US payrolls number released at 1:30 GMT. According to market convention, if not reality, this would be an important barometer of the health of the US economy and might also have a bearing on central bank policy. However, there have been many such moments of tension and anticipation in the past. The trouble is that, on an intra-day basis, they cannot be accurately hedged. If you were short a 1-month straddle and kept hitting the bid or offer in an attempt to hedge, there would be large gaps in your fills. If you delta-hedged once a minute, you would miss the move. If you hedged whenever the underlying moved by 0.5 standard deviations, you might only get filled at the tail end of the spike. In either case, your delta hedging profits would be dwarfed by continuous repricing of the short straddle.

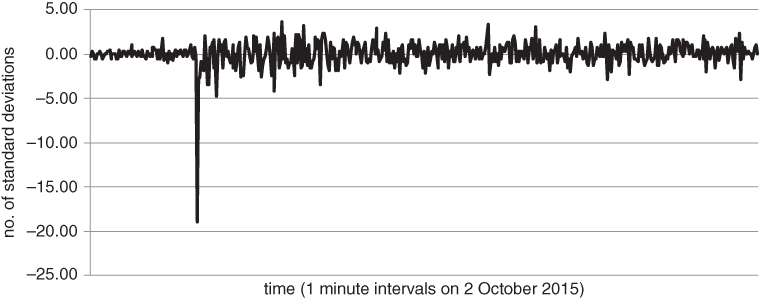

Figures 3.12 and 3.13 rely upon two days of historical data, 1 October and 2 October, 2015. On 1 October, we calculate the standard deviation sigma of 1-minute returns from 7 am to 4:15 pm Eastern Standard Time. On 2 October, we take the same time window and divide each 1-minute return by yesterday's sigma. We have quantified each 1-minute return relative to a 1 standard deviation move on the previous day. The first graph shows 1-minute moves in sigma units for S&P 500 Emini futures.  Figure 3.12 Normalised S&P 500 1-minute moves, 2 October 2015

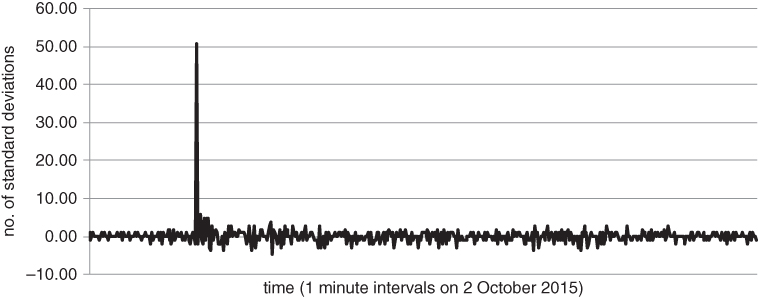

Figure 3.12 Normalised S&P 500 1-minute moves, 2 October 2015  Figure 3.13 Normalised 1-minute moves for US 10 year note futures, 2 October 2015

Figure 3.13 Normalised 1-minute moves for US 10 year note futures, 2 October 2015

The second shows normalised 1-minute moves for US 10 year Treasury note futures, over the same period. The scaling mechanism is the same as above.

HEDGING OPTIONS WITH OTHER OPTIONS

It should be evident that delta hedging is not reliable when volatility changes or there are exaggerated jumps in the underlying asset. The problem compounds when we examine options that have outsized gamma or vega. Such options are highly sensitive to unexpected events. As the saying goes, very short-dated ATM options are “gammatastic”. They have lots of gamma. Near the strike, delta changes rapidly as a function of the spot price. This forces radical rebalancing of the delta hedge, especially if the spot jumps or oscillates wildly around the strike. At the other end of the spectrum, long-dated options are rich in vega. Changes in risk aversion levels can sometimes propagate far along the volatility term structure. If implied volatility increases, long-dated option prices can jump even if there is no material move in the spot. There is no direct way to hedge changes in implied volatility using the underlying alone. This is especially true when implied and realised volatility do not move in tandem. Does this mean that we should never short options that are very close to or very far from maturity? Not necessarily. We can protect against damaging losses without resorting to dynamic hedging. Haug and Taleb (2007) stridently argue that the most direct way to hedge options is with other options. This approach helps you to control all of your Greeks simultaneously. In some sense, it transcends the Greeks, as you can completely eliminate extreme event risk by hedging with options.

Once you sell a vanilla option, you are short gamma and vega. If you buy another option to hedge, some of your gamma and vega might cancel out. Suppose the S&P 500 is trading at 2000 and you want to sell a 1-week 1950 put. While delta might initially be low, it will increase at an accelerating rate if the spot comes anywhere close to 1950. This might force you to bail out of the trade. Alternatively, you could delta hedge the position aggressively, but this would leave you vulnerable to a sudden reversal in the spot. As we will see in Chapter 7, vicious reversals are common in declining markets. A prudent strategy, then, is to buy a lower strike put against the short 1950 put. You might, for example, buy the 1-week 1900 put to cover extreme downside risk. This caps your loss at 50*(contract multiplier), while obviating the need for dynamic hedging.

Once you cover the extreme risk in a structure, you can hold the structure indefinitely without worrying that you will be wiped out. Experienced options traders will affirm that it is easier to extract alpha from a trade you can hold on to. The example above allows you to collect premium with bounded risk. Trading spreads allows you to move away from continuous monitoring of delta, gamma, vega and other Greeks. You don't have to worry quite so much about the path taken by the underlying asset. What is more important is the payout achieved over a given horizon for a range of moves in S and sigma. The tail of the underlying return distribution is now irrelevant, as you have truncated it with the 1900 put. You simply need to decide whether the spread offers good value as a unit.

PUT AND CALL SPREADS

Let's examine option spreads in more detail. They reduce the need for active delta hedging and represent an efficient way to express a targeted view. As above, suppose you think a particular asset is about to go up. This time, however, your conviction level is not quite so high. Rather than buying an outright call or selling an outright put, you can trade a spread. The spread gives you some directional exposure, but does not benefit fully from a large-scale move. To initiate a call spread, you buy a call with a given strike and sell another call with a higher strike. Selling the high strike reduces costs, but also caps your potential gain, as Figure 3.14 suggests. Selling a put spread has the opposite effect. When you buy a low strike put to cover another put that you have sold, you eat into the premium collected while putting a floor on your loss. In the US, put and call spreads are sometimes called “vertical spreads”. The name implies that you buy and sell options at different levels (i.e. strikes), while keeping time, the horizontal dimension, fixed. Call and put spreads can also arise as part of an active trading strategy. You could for example buy a put on a stock index and then sell a lower strike put if the index drops sharply. This allows you to lock in a profit by selling a rich put, while maintaining some level of protection. Conversely, if US 10 year note futures spike and you are short a call, you can buy a further out of the money call to cover your extreme risk. In this way, you can hang on to your original position, with the expectation of a reversal.  Figure 3.14 Evolution of payout curve for a put spread

Figure 3.14 Evolution of payout curve for a put spread

In the diagrams below, we can see how the payout of a put spread varies as a function of the spot. The payout curve is initially quite shallow, but steepens dramatically between the strikes as we approach maturity.

STRADDLES AND STRANGLES

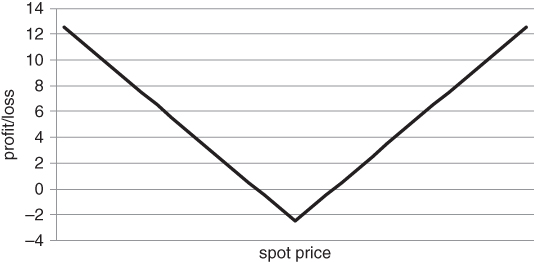

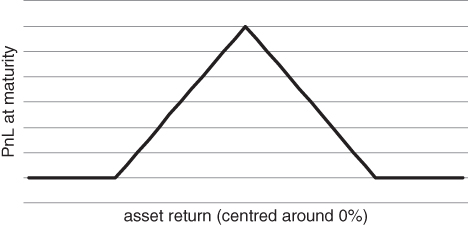

In the previous pages, we have analysed structures that combine a view on volatility with a directional view. But what if we want to make a directionless volatility bet? Option straddles and strangles serve as an entry point into this space. To construct a straddle, you buy an ATM call and put with the same time to maturity. This structure has a symmetric “V” shaped payout profile, as in Figure 3.15.  Figure 3.15 Profit/loss of a straddle at maturity

Figure 3.15 Profit/loss of a straddle at maturity

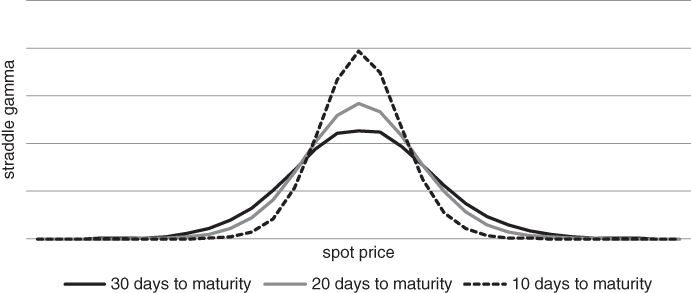

Whether you buy or sell a straddle, the position is initially delta neutral, i.e. the call and put deltas offset. For a moment, let's assume that you decide not to delta hedge the structure. Once the spot moves, the delta will move away from 0, as a function of gamma. If you buy an ATM straddle, you are initially delta neutral, with a long gamma profile. In Figure 3.16, we can see how gamma varies as a function of spot for a long straddle. We have based our calculations on an S&P 500 straddle with 30 days to maturity. As we converge on the maturity date, gamma blows up at the strike and approaches 0 elsewhere, with delta jumping to –1 or 1 for the tiniest of moves.  Figure 3.16 Evolution of gamma curve for a straddle, as time elapses

Figure 3.16 Evolution of gamma curve for a straddle, as time elapses

Gamma peaks at the ATM strike. If the spot initially rises, your delta becomes positive. This can generate material long exposure to the underlying asset. If it falls, you pick up negative deltas. As time passes, you start accumulating delta risk at an ever-increasing rate. Short-dated ATM straddles are packed with gamma, hence should not be shorted in a cavalier fashion. The curve looks a bit pointy at the ATM strike, but this is an artefact of our approximation scheme. Gamma should have roughly the same shape as the probability density function for the underlying asset. In a Black–Scholes world, the gamma profile has a Gaussian, “bell curve” profile.

We can think of things in another way, from the perspective of a straddle buyer. What you really want is a large move one way or another, as your delta-adjusted position size will accelerate in the direction of the move. As time passes, you need a progressively larger move in the spot to break even. This implies that, if you don't delta hedge a long straddle, you need to time your entry and exit points with precision. You can't wait forever for a move to take place. The problem is magnified for straddles that are relatively close to maturity, where theta is largest. Recall that theta is the time decay of an option. If you do decide to delta hedge, straddles transform into a play on the spread between implied and realised volatility. If implied volatility is lower than your forecast of realised volatility, you might buy and hedge a straddle. If it is higher, you might sell and hedge. Since implied volatility usually trades at a premium to realised volatility, selling straddles generally seems to be the more appealing strategy. There are hedge funds and proprietary trading firms that do exactly that. However, if they do not size their positions very conservatively or trade with great skill, they are always in danger of imminent ruin. As we have previously mentioned, large and unexpected jumps in the spot can overwhelm the theoretical edge in a short option position.

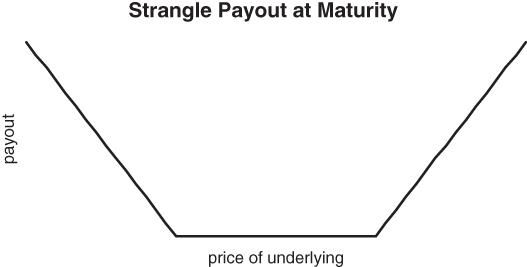

Strangles are the close cousins of straddles. You also buy one call and put per strangle. However, for a strangle, the strikes are spaced apart. In particular, you buy a low strike put and a high strike call to construct a long strangle, as in Figure 3.17.  Figure 3.17 The “strangler” at maturity

Figure 3.17 The “strangler” at maturity

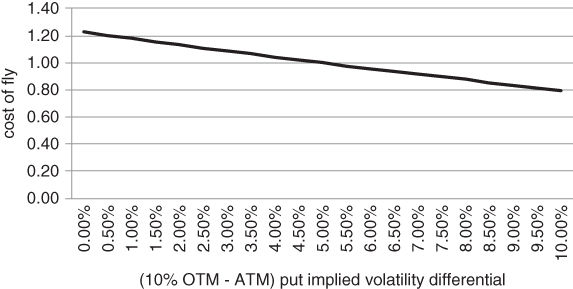

There are a number of reasons to split the strikes and it turns out that some reasons are better than others. Relative to a long straddle, long strangles require relatively low premium outlay. As you push the strikes away from the spot, the cost of each leg in the strangle decreases. Conversely, short strangles can offer value when the implied volatility skew is strongly convex (i.e. when OTM options trade at a significant premium to ATM ones in volatility terms). You then have the opportunity to extract alpha from the relative mispricing of OTM options as well as from high levels of ATM implied volatility. There is another rationale for shorting strangles, although we would recommend against it. Some investors choose to sell strangles rather than straddles in order to “give themselves space”. The strangle delta isn't very sensitive to small moves in the underlying, at least initially. This can give the illusion of safety in a potentially dangerous structure. While your break-even levels might be further away, you need to sell more strangles than straddles to collect the same amount of premium. You either have to settle for lower returns if nothing much happens or apply leverage to the structure, which increases extreme event risk. The concept of giving yourself space would only be appropriate if you knew that there would never be a large move to one side or another during the life of the option. The market does not offer such guarantees. During extreme conditions, the spot can easily crash through one of your strangle strikes, creating more open-ended risk than if you had sold a smaller number of straddles. The payout curve is nice and flat, suggesting that you should make a nearly constant positive return over a wide range of scenarios. However, danger is always around the corner if the structure is not properly attended to.

As we will see in Chapter 4, a wide range of more complex structures also have unbounded risk. By unbounded risk, we mean that there is no nearby limit as to how much you can lose. These include ladders and ratio spreads and may require active delta hedging beyond a threshold. Assuming that you have cut off the extreme downside, however, you can load a position without much active intervention. Sometimes the safe, lazy sod approach is best.

THE DEFORMABLE SHEET

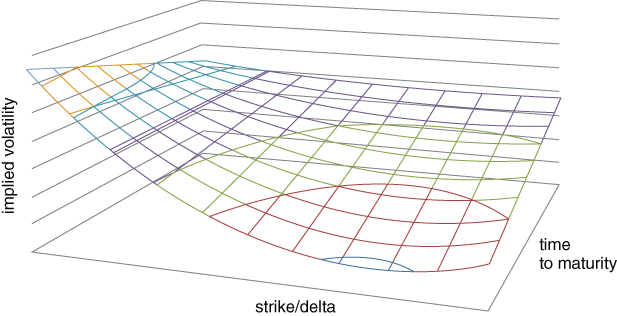

Experienced options traders are able to conceptualise how a given change in short-term ATM volatility will propagate across different strikes and maturities. In our opinion, this is neither voodoo nor special talent, but a learnable skill. The volatility surface moves according to somewhat predictable patterns. Different parts of the surface usually move for logical reasons. For the purposes of hedging, we need to pay particular attention to the “wings”, i.e. low delta calls and puts. In this section, we will briefly describe how the option chain for an asset can be converted into a volatility surface. Note that an option chain is the set of all listed options on a given asset at some point in time. The chain spans different strikes and maturities. We then analyse likely moves at the extremes of the surface conditional on changes in ATM volatility. Whenever an option has a reasonable bid and ask price, we can apply the Black–Scholes transformation to the mid price, converting prices into implied volatilities. The mid price of an asset is simply the average of its bid and ask prices. We wind up with an implied volatility grid, with a value for each strike and time to maturity. After interpolating between points on the grid, we can create an implied volatility surface as in Figure 3.18.  Figure 3.18 Qualitative depiction of an implied volatility surface

Figure 3.18 Qualitative depiction of an implied volatility surface

It is not necessary to define moneyness by strike. In the analysis that follows, we will usually focus on how implied volatility varies as a function of delta. This allows us to adjust for movements in the spot price and volatility over time. There is an ongoing debate over how to model the volatility surface as a function of changes in the spot. We refer the reader to Zou (1999) for further details. In this section, we take a more coarse-grained approach to understanding how the skew might respond to large-scale market moves. The implied volatility surface is difficult to grasp, as it contains so much information. When we start to think about dynamics, the situation gets even worse. There are lots of option prices buzzing around. However, we can sometimes reduce the dimensionality of the problem. If we move one point on the surface a bit, how much should the rest of the surface be expected to move? This is not a purely theoretical question in the context of hedging. In particular, we want to focus on flash points, regions on the surface where volatility is likely to go up the most.

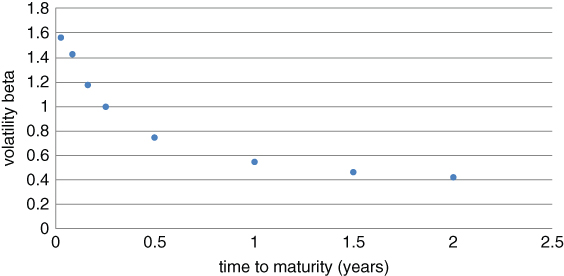

Before looking at dynamics, we can simplify things by looking at static cross sections of the surface. If we focus only on ATM options, we can slice the surface along the y axis. This gives us a curve called the “term structure” of volatility. The term structure reflects market expectations of future volatility over different time horizons. If there is a risk event, short-dated volatility tends to explode, while the rest of the curve moves more modestly. The market is assuming that the event will have diminishing importance over time and prices mean reversion along the curve. Exaggerated moves at the short end can cause the term structure to invert. In Figure 3.19, we focus on S&P 500 options and calculate the beta of changes in ATM option implied volatility for different maturities to changes in 3-month ATM implied volatility. By construction, the beta of changes in 3-month ATM volatility to itself is 1.  Figure 3.19 Variable response of term structure to changes in 3-month implied volatility

Figure 3.19 Variable response of term structure to changes in 3-month implied volatility

If nothing happens after a spike in volatility, short-dated volatility will decline more rapidly than volatility over longer maturities. This is the reverse scenario of what we discussed above. The volatility beta at the short end is relatively high, causing exaggerated movements relative to 3-month volatility. Eventually, the term structure will revert to a more typical, upward sloping shape. Inverted term structures are relatively rare, as bursts in volatility tend to occur infrequently. Bull markets tend to have longer duration than bear markets. However, during prolonged sell-offs, such as in 2008, the curve can remain inverted for quite some time. In summary, short-dated volatility is the dog that wags the long-dated volatility tail. Skew dynamics are more complicated than term structure dynamics, as they are asset dependent. Risky assets, such as equity indices and carry currencies, tend to develop an exaggerated put skew after a market sell-off. Investors are clamouring for downside protection. Other assets can exhibit more complicated dynamics, depending on how the market is positioned and where the need for protection is highest. We examine some of these issues in the next section.

In practice, however, out of the money (OTM) puts and calls are used to construct the matrix. OTM options are generally more liquid, with tighter bid ask spreads. This leads to a more precise implied volatility calculation. OTM option implied volatilities are also easier to calculate in a whippy market, given that their delta is relatively low. As the price of the underlying fluctuates, bid ask spreads for ITM options may not adjust synchronously, causing distortions in implied volatility.

The implied volatility matrix, calculated from OTM options, can be visualised as a surface in three dimensions. The graph below offers a stylised example of an implied volatility surface. The skew is more pronounced for short-dated options and gradually levels out as the time to maturity increases. This is particularly true when we calculate implied volatility as a function of strike, rather than delta. Whereas a 10% OTM put with 1 year to maturity covers moderate downside scenarios, a 10% OTM option with 1 week to go only protects the far left tail. We are effectively looking much further out along the skew when calculating implied volatility for the short-dated OTM put.

From the perspective of long-dated options, strikes that are a fixed distance apart become more similar (in a probabilistic sense) as time to maturity grows. Therefore, the far end of the surface should have a relatively flat skew. In the next section, we give the surface free rein to move, and examine how the put skew for risky assets expands when fear enters the market.

SKEW DYNAMICS FOR RISKY ASSETS

Risky assets, such as equity indices and high yielding currencies, tend to have a put skew. Implied volatility is higher for OTM puts than at-the-money ones. After a drop in the underlying, the put skew tends to steepen, as there is excess demand for disaster insurance. All of this implies that we need to take skew dynamics into account if we want to hedge efficiently.

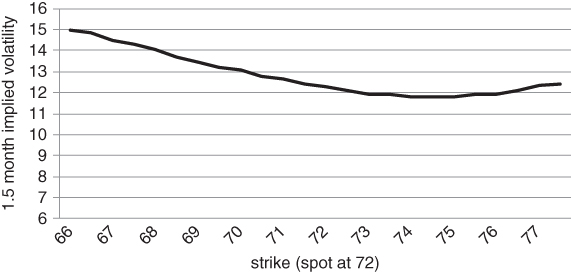

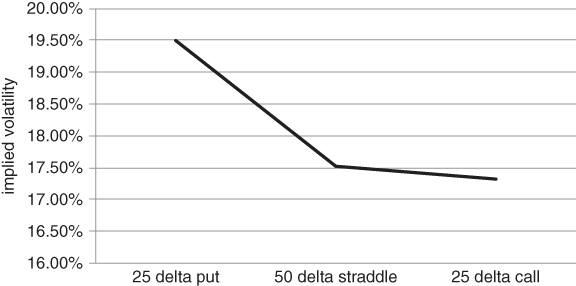

Figure 3.20 gives a snapshot of the implied volatility skew for Australian Dollar futures in late May, 2016. It is representative of the skew for a risky asset under “normal” market conditions. We constructed the skew using OTM calls and puts with roughly 45 days to maturity. In particular, the implied volatility at each strike was derived from an average of the bid and ask price, using the Black 76 formula. The at-the-money strike was 72. To the left of the ATM strike, volatility rises quite rapidly. This suggests that the market was assigning a fairly high probability to a sharp drop in the currency.  Figure 3.20 Implied volatility skew for a risky currency

Figure 3.20 Implied volatility skew for a risky currency

There are a couple of reasons why low delta puts have relatively high implied volatility. On the one hand, risky assets tend to be negatively skewed. The underlying return distribution is more likely to surprise to the downside than to the upside. On the other, there tends to be more structural demand for downside protection. Most investors have a long bias toward risky assets and use options to truncate the distribution of losses in their core portfolios.

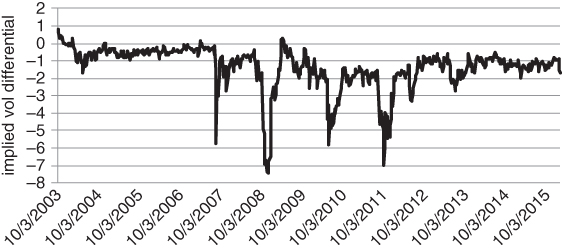

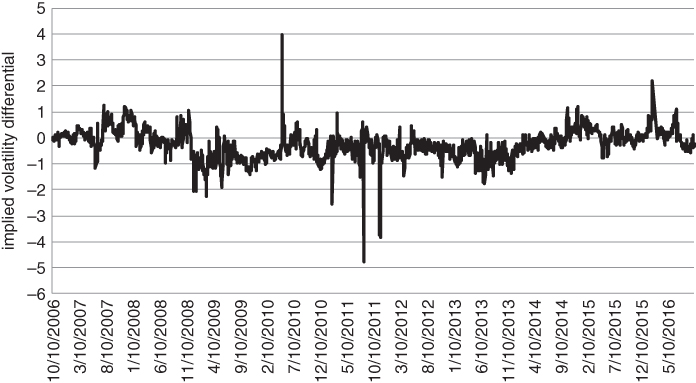

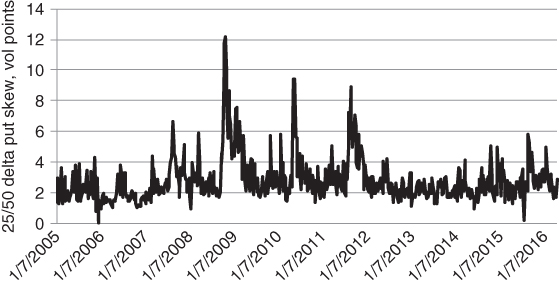

Risky assets have more straightforward skew dynamics than squirrely things like Treasury bonds. They typically have a put skew that becomes steeper as volatility increases. The AUD/USD cross certainly qualifies as a risky asset. The Aussie has historically offered high yield, in exchange for commodity and China risk. In Figure 3.21, we track the 25 delta risk reversal (RR) for the Aussie, relative to the US dollar. Here, the 25 delta RR is defined as the difference between implied volatility for the 25 delta call and put. This quantity is related to the eponymous options structure we described in Chapter 3. For the S&P 500, you might sell a 25 delta put and buy a 25 delta call if the put skew is particularly steep.  Figure 3.21 Negative skewness in the Aussie 25 delta risk reversal

Figure 3.21 Negative skewness in the Aussie 25 delta risk reversal

The dynamics above are quite intuitive. Whenever there is a risk event, the risk reversal drops sharply. Volatility soars across all strikes, with OTM put volatility rising by a disproportionate amount. In other words, the put skew has become elevated. The Aussie tends to plummet during a risk event, with investors nervously paying up for downside protection. Accordingly, we see sharp moves during October 2008, March 2010 and the 2011 European crisis. We also observe that the Aussie RR is nearly always negative. Buying the Aussie is a “yield hog” play. Many investors want a steady source of income. If nothing much happens, they collect. This implies that speculators are biased toward buying the currency and periodically need to buy puts to guard against disaster.

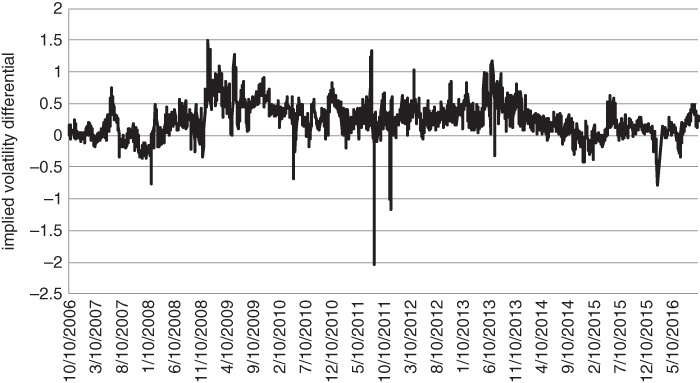

Conversely, if we fix the time to maturity and slice across different option deltas, we get something called the implied volatility skew. The skew is more difficult to characterise than the term structure, as its shape can vary quite dramatically across markets. Equity indices generally have a put skew, as sell-offs tend to be faster than rallies and there is more institutional demand for hedging long portfolios. It has been observed that the put skew became more prominent for equities after Black Monday in 1987. For sovereign bond markets, such as US treasuries, the situation is more complex. In Figure 3.22, we track the difference between 25 delta call and 25 delta put implied volatility over time, using 1-month US 10-year note futures options.  Figure 3.22 Unpredictable skew dynamics for US 10-year futures

Figure 3.22 Unpredictable skew dynamics for US 10-year futures

Ex ante, you might expect there to be a persistent call skew, as treasuries tend to rally during a crisis. As it turns out, the US 10-year skew is a bit of a chameleon, flipping from a call skew to a put skew as risk aversion levels and inflation expectations change over time. When the major risks are inflationary, a put skew might develop. Rising inflation generally leads to rising yields. You can roughly decompose the yield on a bond into one component that measures inflation expectations and another that compensates an investor for bearing duration risk. Conversely, if the market is pricing tough times ahead, a call skew might develop.

THE 1×2 RATIO SPREAD AND ITS RELATIVES

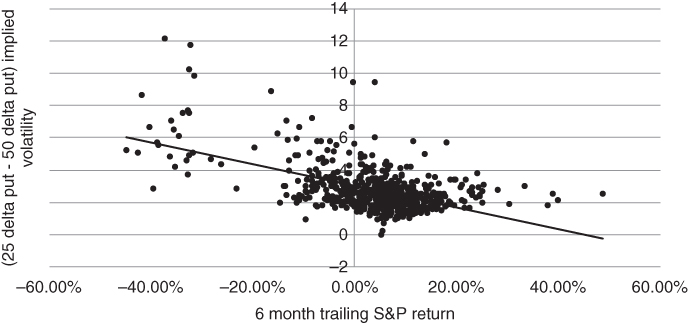

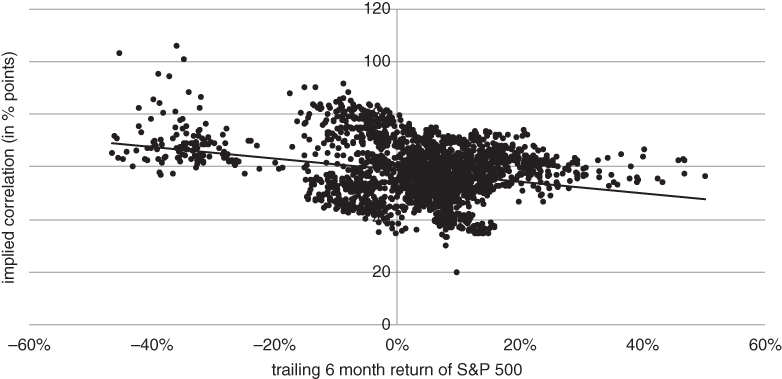

The first skew trade we will examine is the 1×2 ratio spread. This has two varieties, one for calls and one for puts. To construct a call ratio, you buy 1 call that is close to ATM and sell 2 higher strike calls against it. For a put ratio, you buy 1 close to ATM put and sell 2 lower strike calls against it. For example, you might buy 1 US 10-year call at 130 and sell 2 132 calls to build a call ratio. The maturities would generally be the same for both strikes. We will focus on put ratios for now, as they tend to be particularly interesting when analysing the equity index skew. Many traders love to buy 1×2 put ratios when the put skew becomes steep. Market convention dictates that you are long on the 1×2 when you buy the 1 to sell the 2. Suppose the S&P 500 drops sharply. Then, OTM put prices will become elevated, as hedgers enter the market. In all likelihood, the spread between OTM and ATM put implied volatility will increase. In Figure 3.23, we regress levels of the (OTM–ATM) implied volatility spread against the trailing 6-month return for the S&P 500.  Figure 3.23 Dependence of S&P skew on 6-month trailing move

Figure 3.23 Dependence of S&P skew on 6-month trailing move

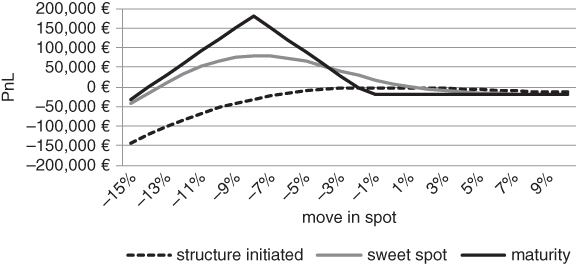

A direct way to mine the skew after a sell-off is to buy 1 ATM put and sell 2 OTM puts, while maintaining delta neutrality. For example, you might buy a 50 delta put and sell 2 25 delta ones when you initiate the ratio. The delta of the “combo” is 0, i.e. . This trade has some interesting properties that are not immediately obvious. In general, you are likely to be a net payer of premium when you enter the trade, yet the structure has positive time decay until you get close to maturity. How can this be possible? When you buy an outright put or call, paying premium implies that you are short theta. Every day that passes without incident, some of the premium erodes from your option. Here, the situation is more complex. If nothing much happens, the 2 25 delta puts will initially burn off faster than the single 50 delta one. You are also likely to benefit from a flattening of the skew if the spot hovers around its current level. This suggests that the passage of time will work in your favour until you get close to expiration. While it is true that you will abruptly become short theta close to expiration, the standard strategy is to roll out of the trade before that point. In the graph below, we show how the payout profile for a long ratio spread evolves as a function of time. Our example is based on Euro Stoxx 50 puts. In particular, we have bought 100 of the 50/25 delta put ratio with about 2 months to maturity. The payout curve is graphed as a function of spot on 3 different dates. The dotted line shows the payout at initiation. The grey “sweet spot” line reflects the time we plan to roll the structure, namely 2 weeks before maturity. Here, the range of positive outcomes is relatively large. For reference, the black line gives the payout at maturity. We have not included the extreme downside in Figure 3.24. However, the structure seems well positioned for a wide range of scenarios.  Figure 3.24 “Safe” zone for a long 1×2 put ratio

Figure 3.24 “Safe” zone for a long 1×2 put ratio

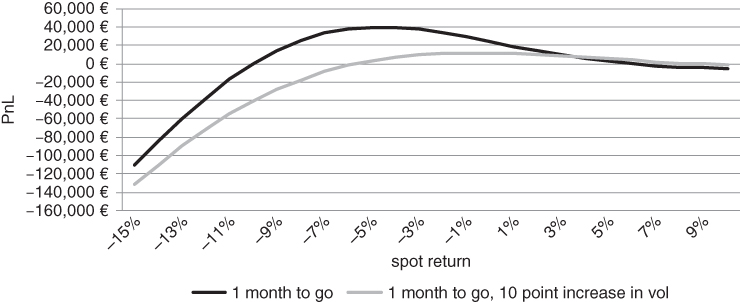

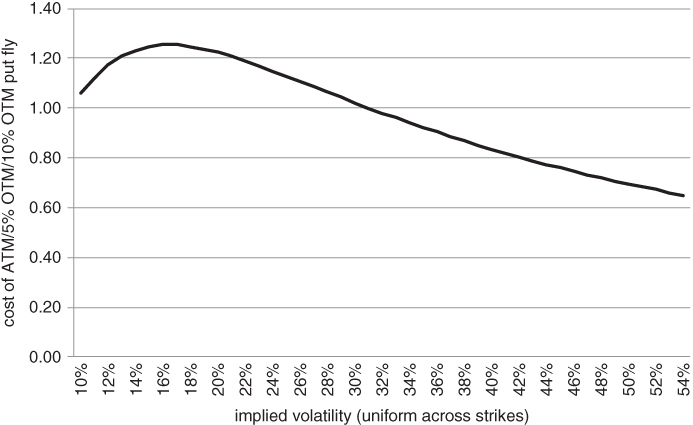

This is a nice-looking trade at some level, but can be fraught with danger. As we will see more acutely in the “Batman” trade section, the trouble is that 1×2 ratio spreads have large vega and extreme event risk. Your loss is essentially open-ended. The 1×2 above is initially delta neutral, as the individual legs cancel each other out for small moves. At first sight, it appears to make money for a wide range of moves in the underlying. However, if there is a severe sell-off, your position converges to a long position in the spot. You are potentially facing a large mark-to-market loss and your delta-adjusted position will have grown dramatically. We can see the embedded volatility risk in Figure 3.25. The graph compares the payout curve with 1 month to go in two scenarios. In the first, volatility remains constant. In the second, there is a parallel shift of 10 points in Euro Stoxx implied volatility. This is not an unusually large shock to the skew. If anything, it understates risk, as the skew is likely to steepen if volatility increases across the board. The window of profitability practically disappears and you are left waiting for a sharp drop in volatility before the next potential sell-off.  Figure 3.25 Sensitivity of 1×2 put ratio to a spike in volatility

Figure 3.25 Sensitivity of 1×2 put ratio to a spike in volatility

It might be argued that you can defend against large moves in the S&P 500 because a circuit breaker will be triggered if the futures drop by a large amount. In theory, you could then hedge or exit the structure. This turns out to be a feeble argument. The reality is that options market makers might pull their quotes during a crash, leaving you with no idea as to where the should be trading. Volatility may have increased to the point where your structure is severely off side. This brings us to an idea that we will explore later in the book. Since s seem innocuous but are fraught with danger, it might be worth thinking about shorting them. The fact that virtually no one else wants to should serve as encouragement. No one wants to be a plumber when they are young, yet it can be quite a stable and lucrative career. Given the lack of demand, the short might be reasonably priced after all. Indeed, in Chapter 4, we will track the performance of a specific short ratio spread and demonstrate its effectiveness as an extreme event hedge.

Put and call ladders are similar to ratios, except that you spread the short strikes apart. Rather than buying a 3-month 1×2 2000/1900 put ratio on the S&P 500, you might buy the 3-month 2000/1925/1850 put ladder. More precisely, you would buy 1 2000 put, sell 1 1925 put and sell 1 1850 put. This structure has three distinct legs instead of two, as you buy 1 2000 put and sell 1 1925 put and 1 1850 put against it. You might buy a ladder if you want to spread your short exposure across the skew, rather than focusing on a single strike. In Figure 3.26, we sketch the payout curve of the 2000/1925/1850 put ladder at various points in time.  Figure 3.26 Put ladder payouts, expanded view

Figure 3.26 Put ladder payouts, expanded view

Conceptually, ratios and ladders are nearly identical and exposed to similar risks. They should be bought with appropriate caution.

THE BATMAN TRADE

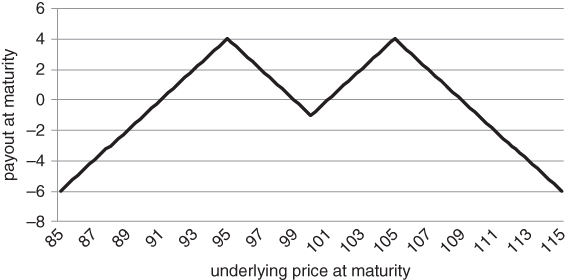

Some trades look pristine from one vantage point, yet very unsightly from another. The 2-sided ratio spread is an excellent example of such a trade. Some traders refer to it as a “Batman” structure, based on the shape of the payout at maturity.

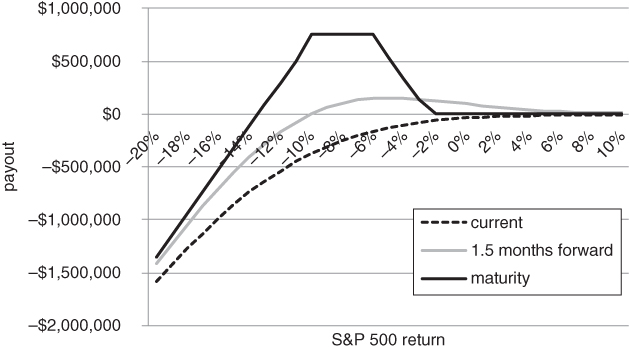

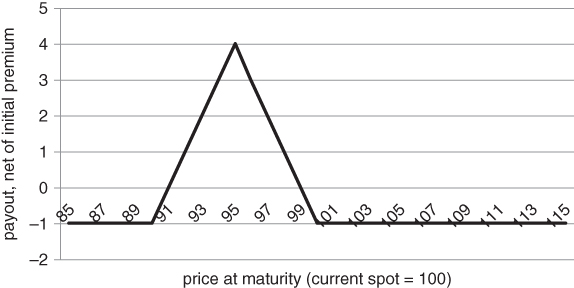

While the Batman logo has changed over the years, Figure 3.27 resembles the original from 1940. The graph below involves buying a 100 strike straddle, while selling 2 95/105 strangles on an asset trading a 100. The structure requires an initial premium outlay and generates a positive payout for moderate up- and down moves.  Figure 3.27 Payout of 2-sided ratio spread (Batman structure) at maturity

Figure 3.27 Payout of 2-sided ratio spread (Batman structure) at maturity

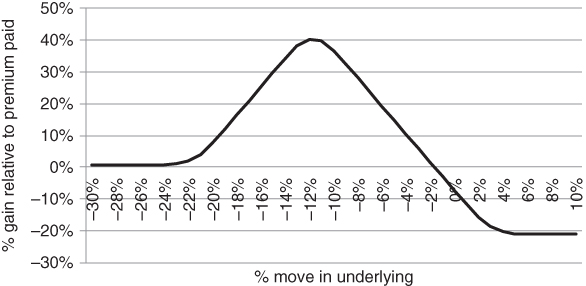

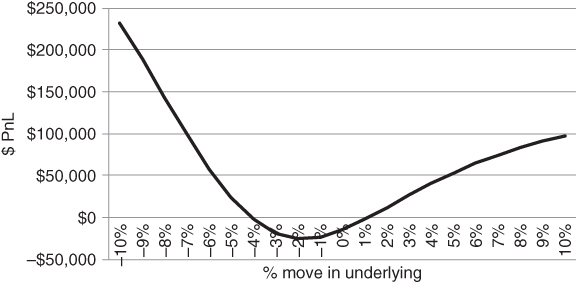

Let's analyse a concrete example. Suppose we initiated the Batman on November 2 2015, focusing on December 2015 futures options. We might buy a 2095 straddle and sell 2 2015/2145 strangles as a relative value play. The straddle/strangle combination can also be thought of as a pair of ratio spreads. We are buying 1 2095 put, selling 2 2015 puts against it, buying 1 call and selling 2 2145 calls against the ATM call. We have chosen the OTM strikes to have roughly 25 delta at the point of trade entry. This ensures that the structure is initially delta neutral. As we will soon realise, the trade is sized aggressively. We have bought 100 straddles and sold 200 strangles on the S&P 500 E-mini futures contract per $1 million of equity. For moderate-sized moves, the payout on 10 December looks nice and flat. If anything, the trade seems bearish, as you make more if the index trickles down over a 5-week period.

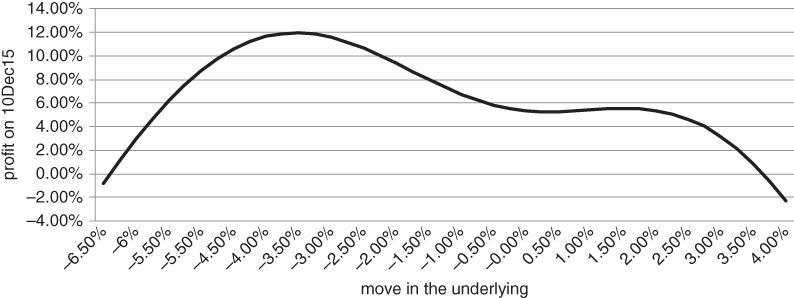

Viewed through this lens, the trade appears to be a winner. Given intermediate returns in the [–6.50%, 4%] range, the expected return of the strategy is strongly positive as shown in Figure 3.28.  Figure 3.28 Profit/loss profile over a range of benign scenarios

Figure 3.28 Profit/loss profile over a range of benign scenarios

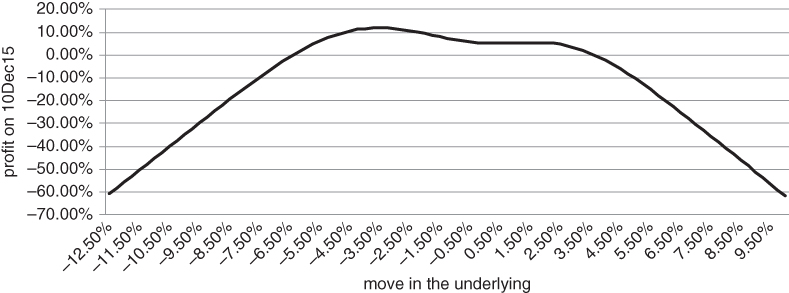

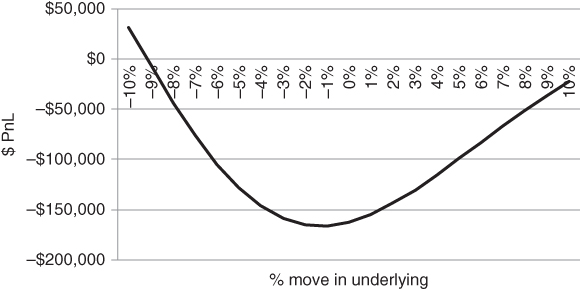

Once we widen our perspective, however, the Batman trade looks far less attractive. Judging from Figure 3.29, potential gains are meagre relative to extreme event losses. The structure is “safer” than a naked straddle, as you have a bit of space to work with when hedging. However, it still has severe open-ended risk.  Figure 3.29 Batman payout: expanded view – the dark underbelly of ratio spreads

Figure 3.29 Batman payout: expanded view – the dark underbelly of ratio spreads

We observe that the Batman trade falls neatly into one of the categories outlined in Taleb's “Anti-Fragile”. The structure likes a bit of disorder, i.e. a certain amount of movement away from the middle strike. However, too much disorder is evidently destructive.

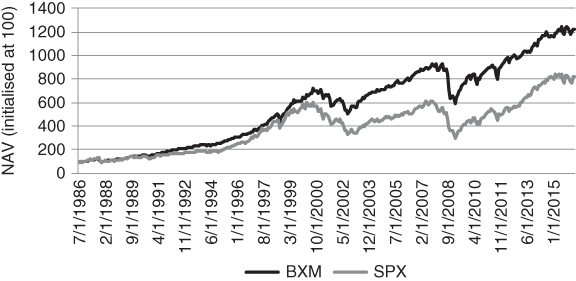

Now we can see the dangers lurking outside of our quiet little settlement. If we have a large balance sheet to support this sort of trade, we should be able to harvest a moderate amount of alpha over the long term. However, we can't push things too hard. The situation is analogous to covered call writing, which might be more familiar to the reader. Covered call writing is sometimes referred to as a “buy-write” strategy. This is a succinct description, as you buy an equity index and write a call against it. Writing is synonymous with selling in this context. Buy-write strategies have been served up as alpha generators for many years (Feldman, 2004). However, there is a limit as to how aggressively the call can be sold. Overwriting strategies make for fine back-tests but are not entirely safe. Suppose we own the S&P 500 (see Figure 3.30). We could, for instance, write 2% OTM calls against our long index position. This would allow us to collect some income each month, with limited participation in S&P rallies. In particular, we would capture premium from the short call and up to 2% from gains in the index. In a bear market, our open-ended risk would be the same as the index. However, we would expect to collect a relatively large amount of premium from the call, as implied volatility would be high. This would reduce a string of monthly losses by a small, but ever-increasing amount. The BXM index, which tracks the performance of this strategy, is widely quoted and has outperformed the S&P 500 on a risk-adjusted basis since inception.  Figure 3.30 Performance of buy-write strategy relative to static long position in index

Figure 3.30 Performance of buy-write strategy relative to static long position in index

What is generating alpha in the buy-write? It must be the short call component, as our position is otherwise identical to the benchmark. The short call has negative correlation to the index, as its delta is always less than 0. It also benefits from the tendency of implied volatility to be an overpriced relative to realised volatility, in the absence of an extreme event. This leads to a thought. If the short call is responsible for all of the alpha, why don't we trade it on a stand-alone basis? While tempting, this idea is not a particularly good one. If we start a hedge fund that sells calls willy-nilly, we no longer get the diversification effect from owning the index. We also have to sell a large number of calls to achieve a decent return. In an environment where interest rates are close to 0, there is nowhere to hide. We don't receive any return for excess cash held at our prime broker. As a consequence, we will probably have to use substantial leverage if we want to produce a decent-looking nominal return. The trouble with this idea is that, if equities ramp up, our risks will escalate. We might be forced to buy back the calls at a significant loss. By contrast, if we were simply selling calls against a well-capitalised long position, our delta-adjusted risk would actually drop after a sharp index rally. We might underperform that month, but would have the firepower to reload the strategy indefinitely.

Let's move back to the Batman. Suppose that we only bought 10 Batman structures per $1 million of equity (scaling the trade down by a factor of 10). Then, we might be able to absorb the occasional large drawdown without having to react aggressively. However, this would only allow us to target a return of 50 to 60 basis points every time we loaded the structure. As soon as we force things, adding leverage in an attempt to boost returns, we are vulnerable to short-term price moves in the underlying.

IMPLIED CORRELATION AND THE EQUITY INDEX SKEW

This book unashamedly has a macro bias, based on the author's background and investment philosophy. However, we try to redress the balance slightly here. We have spoken at length about equity index volatility while saying nothing about the volatility of the components of the index. This might seem strange at some fundamental level. Indices would not exist without the assets that underpin them. However, the evidence suggests that stocks move together at moments that matter the most.